One-third (33%) of Australians see incomes fall due to the onset of COVID-19, according to a recent ME Bank survey. The finding suggests:

- 20% of Australians have taken a wage cut;

- 17% have lost their job; and

- 29% are feeling “insecure about their job”.

Moreover, 63% of Australians cited serious concerns over the economy as a primary driver of negative financial outlook. People are rightfully wondering “how long will my money last” through this COVID-19 crisis.

You can use our COVID-19 savings calculator above to help you determine that. It also helps you understand how taking a repayment holiday can help you build a savings buffer.

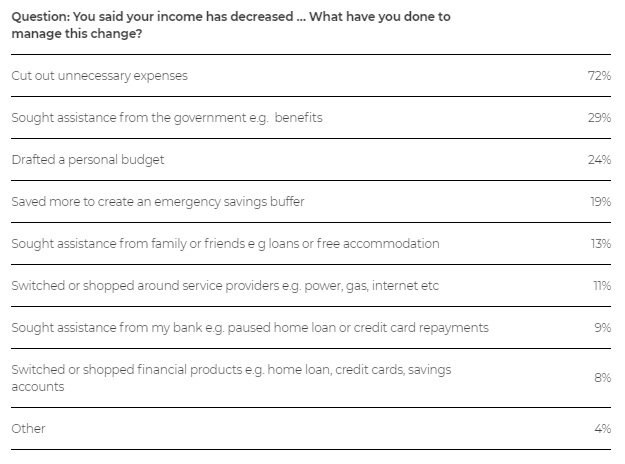

How are Australians managing their finances with reduced income?

Let’s look at all these strategies a bit closely.

1. Cut out unnecessary expenses

The lockdown and the social distancing measures have forced us to stay at home, curtailing much of our discretionary spending on eating out, movies, holidays etc. This has forced us to save more.

Making lifestyle changes is a much harder proposition than we anticipate, i.e. once we’re used to a certain premium/luxury product, going back to normal is hard. But worth it as far as savings are concerned.

In the past, cutting down on unnecessary living expenses enabled many of our customers to save a house deposit. You can use the same strategy to build up a savings buffer.

2. Seek financial assistance from the government

These are unprecedented times that come around once in a lifetime. As evident from Centrelink’s online portal crashing as hundreds of thousands of Australians sought help amidst the coronavirus pandemic.

The government’s financial assistance for individuals and households includes:

- Coronavirus supplement of $550 per fortnight over the next 6 months. This will be paid to both existing and new recipients of JobSeeker Payment, Youth Allowance Jobseeker, Parenting Payment, Farm Household Allowance and Special Benefit.

- JobKeeper payments of $1,500 per fortnight. The JobKeeper payment helps businesses significantly impacted by the Coronavirus cover the costs of their employees’ wages, so more Australians can retain their jobs and continue to earn an income. Your employer will notify you if they intend to claim the fortnightly payment of $1,500 on your behalf.

- Two separate $750 payments to social security, veteran and other income support recipients and eligible concession cardholders. The first payment will be made from 31 March 2020 and the second payment will be made from 13 July 2020.

- Temporary release of superannuation. Access up to $10,000 of their superannuation in 2019-20 and a further $10,000 in 2020-21. Individuals will not need to pay tax on amounts released, and the money they withdraw will not affect Centrelink or Veterans’ Affairs payments.

Using anonymised banking transaction data of hundreds of thousands of Australians, the illion and AlphaBeta data shows that, within a fortnight, nearly half (43%) of the stimulus money has already been spent by its recipients.

and AlphaBeta data")

The government has also announced several stimulus packages to help business owners cope with the economic fallout of the coronavirus pandemic.

One of them is the SME guarantee Scheme under which eligible businesses can get a loan up to a maximum of $250,000.

Under this scheme, loans terms can go up to three years, with an initial six-month repayment holiday. Moreover, businesses will not be required to provide an asset as security for the loan.

3. Draft a personal budget

To create a basic personal budget:

- Note down your net income (after tax and deductions, that is your take-home pay.

- Track your expenses and spending. Identify where you can cut expenses.

- Set your goals.

- Make a plan and stick to it.

- Adjust your habits. Remember, there’s a difference between wants and needs.

- Regularly check-in to see if you’re sticking to your budget.

You can also look for a free budgeting app online to help you track your income and spending.

4. Saved more to create a savings buffer

So, how much should you save as emergency funds? Some recommend that one should have emergency funds to cover at least 3 month’s living expenses set aside. While others recommend having a 6-month or even a 12-month buffer. Ultimately, the exact amount will depend on your financial situation and lifestyle.

5. Seek assistance from friends and family

Moving in with their parents or friends is something people have done to save money on rent. It may be worth considering moving in or asking for a loan to help through this crisis. Although not everyone will have this option. Alternatively, different states have announced rent relief measures. You may be able to negotiate rent reduction if you’ve been financially affected by COVID-19. Please refer to your state government website for more information.

6. Shop around for “better value” service providers

Now it’s a great time to see if you can cut the cost of energy, internet and phone bills. Review your bills, and look for opportunities to cut cost. There are offers to be had! Do you have a subscription to a number of streaming services? Go over your subscriptions to identify where you can cut down. Close off services that you’re not using (eg gym memberships, etc) Most utility providers and councils have hardship officers that can help you work out a plan to pay the bill in instalments.

There are also rebates and vouchers that can help you pay your utility bills. This list breaks down what vouchers are available and where to apply for them.

7. Freeze your mortgage repayments

Home loan customers with most lenders are able to freeze their mortgage repayments for up to 6 months as part of COVID-19 mortgage relief announced by lenders.

Even lenders who don’t have a COVID-19 specific relief package have financial hardship arrangements in place, as mandated by law.

So please get in touch with your lender or your mortgage broker, to go over your options which may include:

- Freezing your mortgage repayments with a repayment holiday.

- Switching to interest-only repayments to reduce your repayments.

- Accessing equity to help manage your cashflow.

- Debt consolidation to make repayments manageable.

- Extending the loan term to reduce your repayments.

- Utilising funds in redraw or offset accounts.

8. Shop for a better deal, e.g. home loan, credit cards, savings accounts

Mortgage interest rates are at record lows. For some, refinancing to a home loan with a lower interest rate and immediately freezing your mortgage repayments can help you save on interest as well as manage your finances.

Shop around for a savings account with low fees and a competitive interest rate. Online savings account sometimes have highly competitive rates. However, please carefully go through the terms and conditions before making the switch.

9. Other strategies

Accessing $20,000 from your superannuation

As a result of COVID-19, the government has announced that financially affected Australians can withdraw up to $10,000 from their super early this financial year (before 30 June 2020) on compassionate grounds or financial hardship. And another $10,000 in the next financial year which starts on 1 July 2020.

To be eligible to withdraw from your super early, you typically need to have been receiving social security benefits for at least 6 months. However, withdrawing super early could have a big impact on your long term retirement amount. Industry Super Australia (ISA) looked at the numbers and that for a person aged 30 withdrawing $20,000 could have a difference of $97,214 at retirement. The younger you are the bigger the difference at retirement!

Review your insurance

Review and compare your insurances to see if you’re getting the best deal:

- Health insurance

- Car insurance

- Home insurance etc.

Look for ways to boost your income

Freelancing or side gigs you can do from home can help you boost your income during this crisis. In fact, many successful freelancers have made the switch to working full time on their side gigs. This list is in no way extensive and is a representation only. You may find other, more efficient ways of managing your finances.

Review your home loan

If you’d like to review your home loan to find out how you may be able to reduce your mortgage repayments or save on interest by refinancing to a lower rate, talk to one of our specialist mortgage brokers.

Call us on 1300 889 743 or fill in our short assessment form to go over your options.